Unlocking the Mystery: Your Guide to the Franklin Collection Service Number

Navigating the world of debt collection can be stressful, and understanding how to contact the specific agency attempting to reach you is crucial. If you’re searching for the Franklin Collection Service number, you’re likely seeking to resolve a debt, understand a communication you’ve received, or clarify your account status. This comprehensive guide provides everything you need to know about Franklin Collection Service, how to reach them, and how to navigate your interactions effectively. We aim to provide clear, reliable information to empower you to take control of your financial situation.

Decoding Franklin Collection Service

Franklin Collection Service, Inc. is a debt collection agency. They work with various creditors to recover outstanding debts from consumers. Understanding their role is the first step in addressing any communication you receive from them. They act as an intermediary, attempting to collect on debts that you may owe to other companies. Their business is inherently tied to the financial health of creditors, and their methods are governed by federal and state regulations, including the Fair Debt Collection Practices Act (FDCPA).

The company’s history reflects the evolution of debt collection practices. Initially focused on traditional methods, they have adapted to incorporate digital communication and data analytics. This evolution allows them to locate and contact debtors more efficiently, but it also necessitates a greater emphasis on compliance and ethical conduct.

At its core, the concept of debt collection hinges on the contractual obligation between a creditor and a debtor. When a debtor fails to meet their payment obligations, the creditor may engage a collection agency like Franklin Collection Service to recover the funds. This process is subject to a complex legal framework designed to protect consumers from abusive or unfair practices.

Identifying Authentic Communication from Franklin Collection Service

In today’s digital age, it’s crucial to verify the authenticity of any communication you receive, especially when it involves financial matters. Scammers often impersonate legitimate businesses, including debt collection agencies, to defraud unsuspecting individuals. Therefore, before engaging with anyone claiming to represent Franklin Collection Service, take steps to confirm their identity.

- Cross-Reference the Number: If you receive a call, search the number online. Legitimate businesses will typically have their number listed publicly.

- Request Written Verification: Under the FDCPA, you have the right to request written verification of the debt. This verification should include the name of the original creditor, the amount of the debt, and other relevant information.

- Check for Consistent Information: Be wary of inconsistencies in the communication. Scammers may use outdated or inaccurate information.

Always be cautious about providing personal or financial information over the phone or online unless you have verified the identity of the party requesting it. If you have any doubts, contact Franklin Collection Service directly using the contact information provided on their official website.

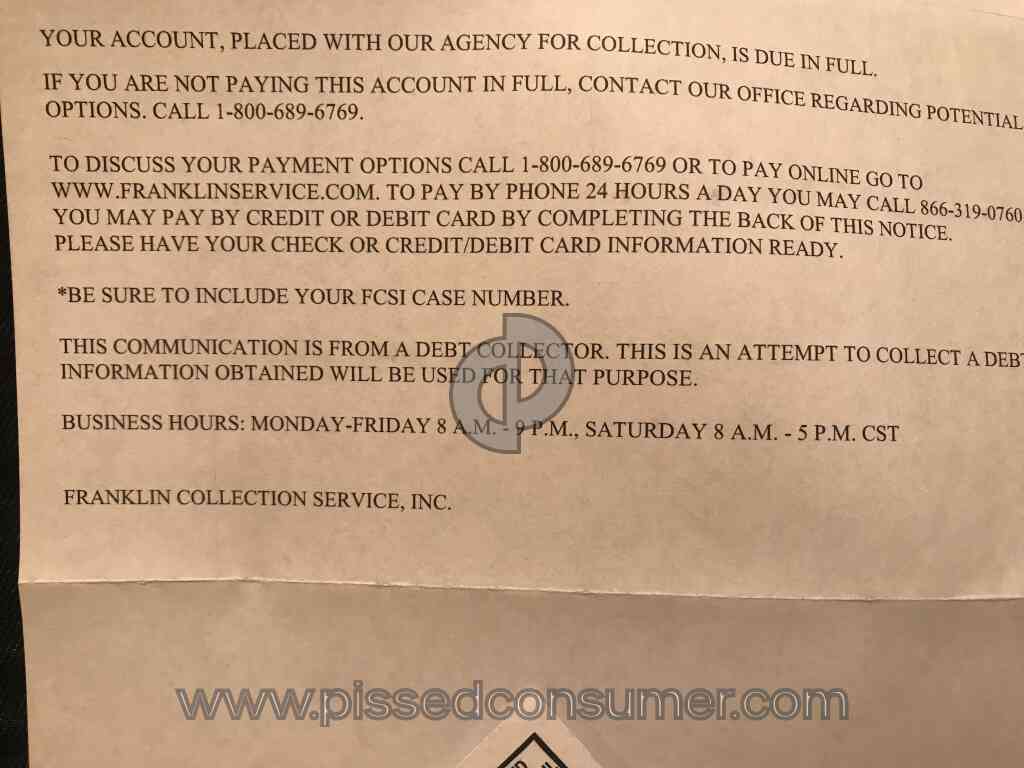

Contacting Franklin Collection Service: Finding the Right Number

Locating the correct Franklin Collection Service number is essential for resolving your debt-related concerns. The most reliable source is their official website. Look for a “Contact Us” or “Customer Service” section, where you should find their phone number and other contact information. Be aware that different departments might have distinct numbers, so choose the one that best matches your inquiry.

It’s also wise to consult reputable online directories, like the Better Business Bureau (BBB), which often list contact information for businesses, including debt collection agencies. However, always double-check the information against the official website to ensure accuracy.

Keep in mind that Franklin Collection Service may have multiple numbers for different purposes or locations. Make sure you’re calling the appropriate number to avoid delays or misdirection. If you’re unsure, start with their general customer service line and explain your specific needs.

Navigating Your Interactions with Franklin Collection Service: Your Rights

Understanding your rights under the Fair Debt Collection Practices Act (FDCPA) is paramount when dealing with debt collection agencies. The FDCPA protects you from abusive, unfair, or deceptive practices. Knowing your rights empowers you to assert them and navigate your interactions with Franklin Collection Service more effectively.

Some key rights under the FDCPA include:

- Right to Validation: You have the right to request written validation of the debt, as mentioned earlier.

- Right to Cease Communication: You can send a written request to the collection agency to cease communication with you. However, they may still pursue legal action to collect the debt.

- Protection from Harassment: Debt collectors are prohibited from harassing, oppressing, or abusing you. This includes making threats, using obscene language, or calling you at unreasonable hours.

- Right to Dispute: If you believe the debt is inaccurate or invalid, you have the right to dispute it. The collection agency must investigate your dispute and provide you with documentation to support their claim.

Document all your interactions with Franklin Collection Service, including dates, times, and the content of conversations. This documentation can be valuable if you need to file a complaint or take legal action.

The Role of Compliance in Franklin Collection Service’s Operations

Compliance with federal and state regulations is critical for Franklin Collection Service’s legitimacy and operational integrity. They must adhere to the FDCPA and other applicable laws, which govern their conduct and protect consumers from unlawful practices. A robust compliance program helps ensure that they treat consumers fairly and ethically.

Compliance involves training employees on the FDCPA, monitoring their communication with consumers, and implementing procedures to address complaints and resolve disputes. It also requires staying up-to-date on changes in the legal landscape and adapting their practices accordingly.

Consumers can play a role in promoting compliance by reporting any suspected violations of the FDCPA to the Consumer Financial Protection Bureau (CFPB) or their state attorney general. These reports can help regulators identify and address systemic issues within the debt collection industry.

Understanding Debt Validation and Verification

Debt validation and verification are crucial steps in ensuring the accuracy and legitimacy of a debt. When you request validation from Franklin Collection Service, they must provide you with certain information, including the name of the original creditor, the amount of the debt, and a copy of the original contract or other documentation that establishes your obligation to pay.

Verification goes a step further. It involves confirming that the debt is accurate and that the collection agency has the legal right to collect it. This may require them to investigate your dispute and provide you with additional documentation or evidence.

If Franklin Collection Service fails to provide adequate validation or verification, you may have grounds to challenge the debt and prevent them from collecting it. It’s essential to understand your rights and assert them if you believe the debt is invalid or inaccurate.

Negotiating a Debt Settlement with Franklin Collection Service

Negotiating a debt settlement can be a viable option for resolving your debt with Franklin Collection Service. A settlement involves agreeing to pay a reduced amount of the total debt in exchange for the collection agency’s agreement to forgive the remaining balance. This can be a mutually beneficial arrangement, allowing you to resolve your debt for less than the full amount while providing the collection agency with a guaranteed payment.

When negotiating a settlement, it’s important to:

- Assess Your Financial Situation: Determine how much you can realistically afford to pay.

- Start with a Low Offer: Begin by offering a percentage of the total debt, such as 25% or 50%.

- Be Prepared to Negotiate: The collection agency will likely counteroffer, so be prepared to negotiate until you reach an agreement that works for both parties.

- Get the Agreement in Writing: Once you reach an agreement, make sure to get it in writing before making any payments. The written agreement should clearly state the amount of the settlement, the payment terms, and the collection agency’s agreement to forgive the remaining balance.

Consider seeking guidance from a credit counselor or attorney to help you navigate the negotiation process and ensure that you get the best possible outcome.

Franklin Collection Service and Your Credit Report

Franklin Collection Service’s activities can impact your credit report. If they report a debt to the credit bureaus, it can negatively affect your credit score, making it more difficult to obtain loans, credit cards, or other forms of credit in the future.

It’s crucial to monitor your credit report regularly to identify any inaccuracies or errors. If you find a debt from Franklin Collection Service that you believe is inaccurate or invalid, you have the right to dispute it with the credit bureaus. The credit bureaus are required to investigate your dispute and remove the debt from your credit report if it cannot be verified.

Even if the debt is accurate, negotiating a settlement and paying it off can improve your credit score over time. However, keep in mind that the negative impact of the debt may remain on your credit report for several years, even after it’s been paid.

Alternatives to Dealing Directly with Franklin Collection Service

While dealing directly with Franklin Collection Service is often necessary, several alternatives can help you manage your debt and protect your financial well-being.

- Credit Counseling: Non-profit credit counseling agencies can provide you with guidance on budgeting, debt management, and credit repair.

- Debt Management Plans (DMPs): A DMP involves working with a credit counseling agency to consolidate your debts and make monthly payments to the agency, which then distributes the funds to your creditors.

- Debt Consolidation Loans: A debt consolidation loan involves taking out a new loan to pay off your existing debts. This can simplify your payments and potentially lower your interest rate.

- Bankruptcy: Bankruptcy is a legal process that can discharge certain debts, providing you with a fresh start. However, it can also have a significant negative impact on your credit score.

Evaluate your options carefully and choose the one that best fits your individual circumstances and financial goals. Consider seeking professional advice from a financial advisor or attorney to help you make an informed decision.

Protecting Yourself from Debt Collection Scams

Debt collection scams are becoming increasingly common, so it’s essential to be vigilant and protect yourself from becoming a victim. Scammers often impersonate legitimate debt collection agencies, using aggressive tactics to pressure you into paying debts that you don’t owe or that are already past the statute of limitations.

To protect yourself, be wary of:

- Threats and Intimidation: Legitimate debt collectors are prohibited from making threats or using abusive language.

- Demands for Immediate Payment: Scammers often demand immediate payment, often by unconventional methods such as prepaid debit cards or wire transfers.

- Refusal to Provide Information: Legitimate debt collectors will provide you with written validation of the debt upon request.

- Calls at Odd Hours: Scammers may call you at unreasonable hours, such as early in the morning or late at night.

If you suspect that you’re being targeted by a debt collection scam, report it to the Federal Trade Commission (FTC) and your state attorney general.

Resolving Your Debt and Moving Forward

Dealing with debt can be challenging, but it’s important to remember that you have options. By understanding your rights, communicating effectively with Franklin Collection Service, and exploring available resources, you can resolve your debt and take control of your financial future. Don’t be afraid to seek help from credit counselors, attorneys, or other professionals who can provide you with guidance and support.

Remember, resolving your debt is not just about paying off what you owe; it’s about regaining your peace of mind and building a stronger financial foundation for the future. Take proactive steps to manage your debt, protect your credit, and create a budget that allows you to achieve your financial goals.

Taking Control of Your Financial Well-being

Understanding the Franklin Collection Service number is just the first step in taking control of your financial well-being. By educating yourself about debt collection practices, asserting your rights, and seeking professional guidance when needed, you can navigate the debt collection process with confidence and resolve your financial obligations effectively. Remember, you are not alone, and resources are available to help you achieve your financial goals. Contact financial experts today for advice tailored to your unique circumstances.